Dell soars its revenue in the first fiscal quarter of 2027 supported by AI servers and maintains focus on business

Dell Technologies has introduced the results of its first fiscal quarter of 2027 with record figures in revenue, profit and cash, driven above all by the infrastructure business for artificial intelligence. The company reported revenue of $43.8 billion, up 88% year over year, along with diluted earnings per share of $5.24 on a GAAP basis and $4.86 on a non-GAAP basis. In parallel, operating cash flow reached $4.1 billion, also at a high for a first quarter.

Dell has insisted that the demand for AI optimized servers It continues to accelerate, to the point that it booked $24.4 billion in AI orders and recognized $16.1 billion in revenue linked to this segment. The magnitude of that figure explains a good part of the group’s jump and also why the company has raised its annual revenue forecast for AI-Optimized Servers to around $60 billion.

It is worth briefly clarifying what GAAP means. In short, GAAP is generally accepted accounting principles in the United States.that is, the standard framework with which companies present their official results. When a company talks about non-GAAP figures, it usually adjusts some extraordinary or non-recurring items to offer a closer view of the operations of the business. The interesting thing in this case is that both metrics show very strong growth, although the GAAP reference would be the most reliable.

Infrastructure pulls the business and the business client remains ahead

The area that sustains the quarter is Infrastructure Solutions Group (ISG), which registered $29 billion in revenue181% more than a year before. Within that division, AI-optimized servers soared 757%, to 16.1 billion, while traditional servers and networking grew 92%, to 8.5 billion. Storage, for its part, advanced 8% and reached 4.3 billion. ISG’s operating profit rose 206% to 3.1 billion.

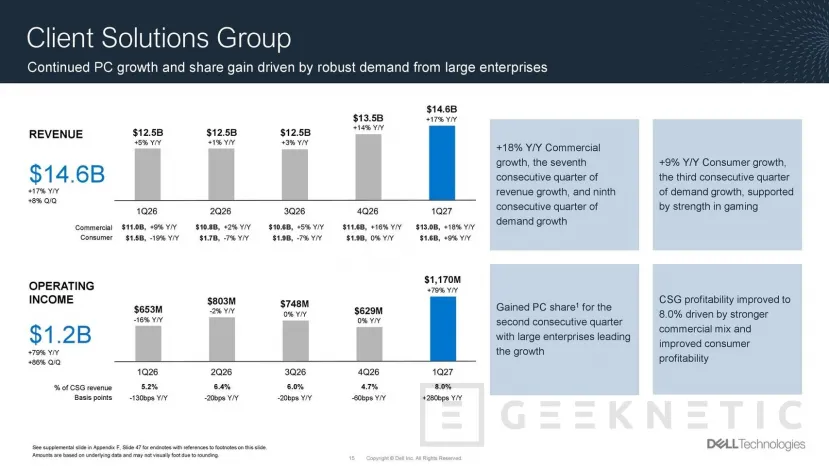

The other large leg of the group, Client Solutions Group (CSG), also improved, although with a much lower intensity. Dell reported revenue of $14.6 billion in customers17% more year-on-year. Within this division, the commercial business contributed 13,000 million, with an increase of 18%, while consumption remained at 1,600 million, growing 9%. The data confirms that the brand continues to depend much more on the corporate client than on the consumer market, something consistent with its positioning, but which also limits the relative weight of that part of the business.

From an IT-oriented reading, Dell’s message is clear. The company wants to present itself as a supplier of complete infrastructure for AI uploadsfrom servers to storage and networking, at a time when many organizations are expanding capacity for training, inference and enterprise deployments. Namely, it’s not just about selling isolated hardware, but rather capturing a larger share of the spend associated with AI-ready data centers.

Very high prospects and still concentrated growth

Looking ahead to the fiscal second quarter, Dell expects revenue between $44 billion and $45 billion, with a midpoint of $44.5 billion. For the entire fiscal year 2027, the guide rises to a range of 165,000 to 169,000 million, with 167 billion at the midpointwhich would mean growth close to 50% year-on-year. The company also expects full-year GAAP diluted earnings per share of $17.31 and non-GAAP earnings per share of $17.90.

Now, it is also time to be cautious. The great engine of the quarter is back very focused on AI and in particular servers. Therefore, a relevant part of the boost depends on this demand continuing to maintain the expected pace. Furthermore, although consumption is growing, it is doing so from a much more modest base than that of the commercial business. In other words, the company has a very positive quarter, but it also shows that its current expansion cycle is especially linked to the strength of business investment in AI infrastructure. As long as the market follows this demand trend, Dell remains strong in the face of a possible purchase by a company like NVIDIA, which, for now, has denied that this is the intention.